What “Settlement Layer” Really Means in Finance

It sounds like the most boring word in finance. Its actually the bedrock everything stands on and the dirty secret is that when you hit “buy” or “pay,” nothing has really moved yet.

This is a deep-dive into the bottom floor of the new financial stack. New to the vision? Start here → One Planet, 180 Currencies. Something’s Off.

Im going to ruin a word for you. After this, you wont be able to hear “settlement” the same way again and that’s the point, because its quietly one of the most important words in all of finance, and almost nobody outside the industry actually knows what it means.

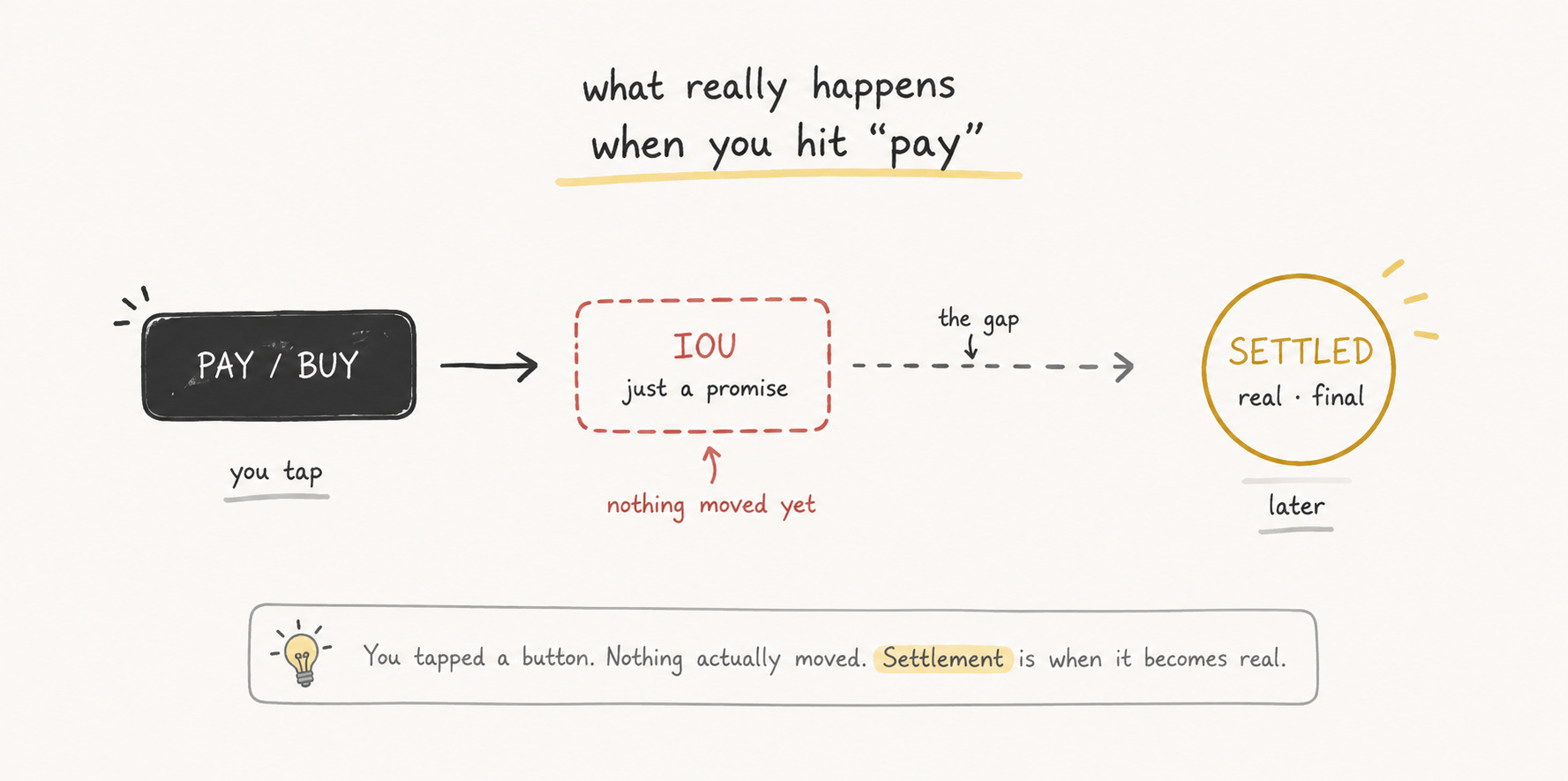

Lets start with something that should unsettle you a little. Right now, when you tap “pay” on your phone, or hit “buy” on a stock... nothing has actually moved yet.

Read that again. The money didnt go anywhere. You dont own the stock. What you did was send a message - a promise, an instruction, an IOU. The actual moving of value - the real, final, irreversible handover - happens later. Sometimes seconds later. Often a full day later. Sometimes days. That moment when it finally becomes real has a name. Its called settlement.

This gap between the promise and the real transfer is invisible to you, but its the hidden foundation that all of finance is built on. And understanding it is the key to understanding why the old system is slow and quietly dangerous, why a famous meme-stock frenzy got shut down, and why the most powerful institutions on earth are rebuilding finance from this layer up. So lets decode it properly.

Two words everyone confuses

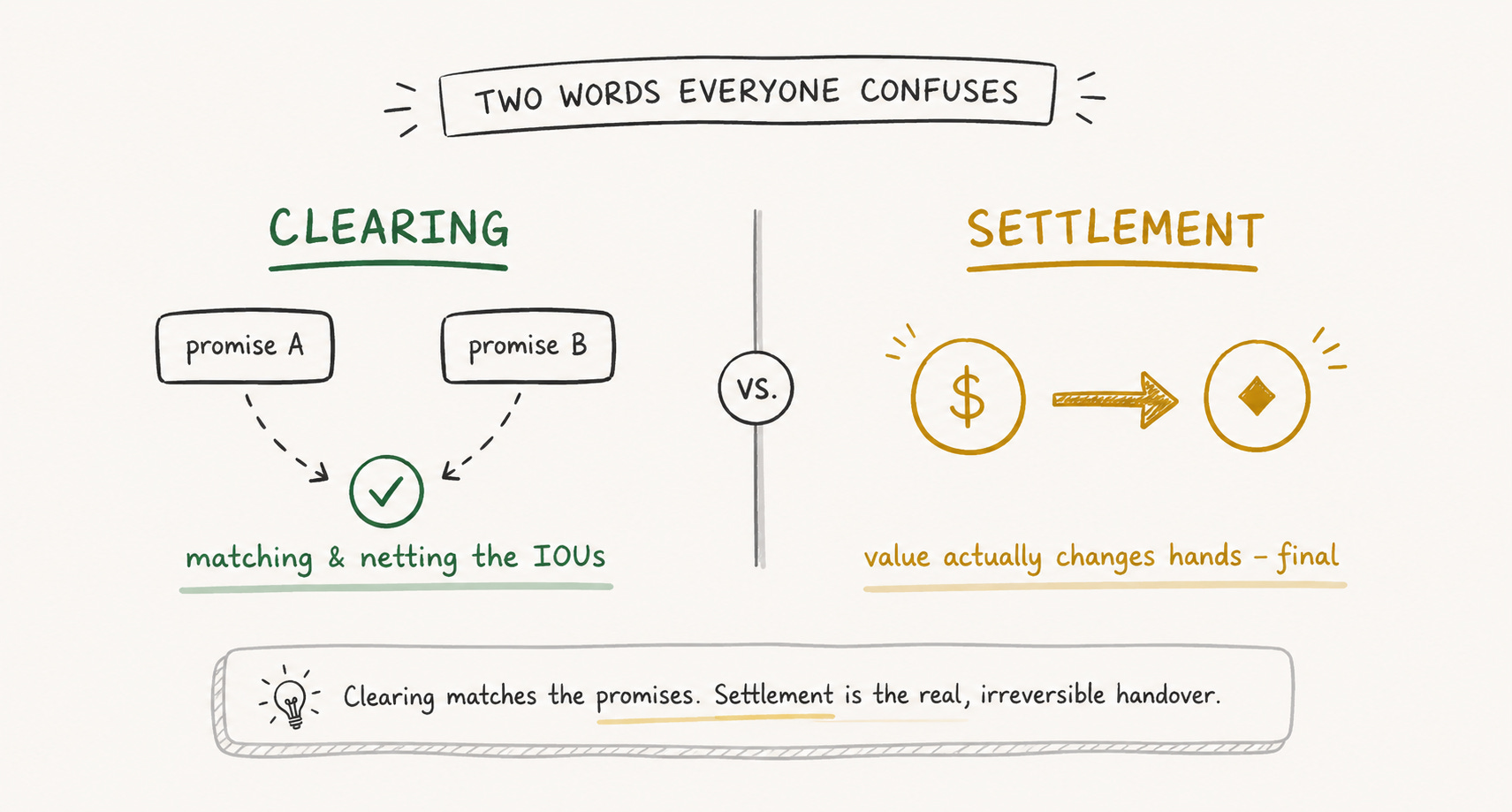

First, untangle two words that get used interchangeably but mean very different things: clearing and settlement.

Clearing is the paperwork. When you trade, a middleman steps in to match the two sides, check that everyone is good for it, and net everything out - figuring out who owes what to whom. Its the organizing of all the promises. Settlement is the real thing: the actual moment the money and the asset change hands, finally and irreversibly. Clearing is agreeing on the deal. Settlement is the deal actually happening.

Everything you do in finance is really these two steps - a promise, then (later) the settlement that makes it real. The whole question is: how long is the gap in between? And who is exposed while it sits open?

The gap, hiding in plain sight

Heres where it gets uncomfortable, because the gap is bigger than you think even in 2026.

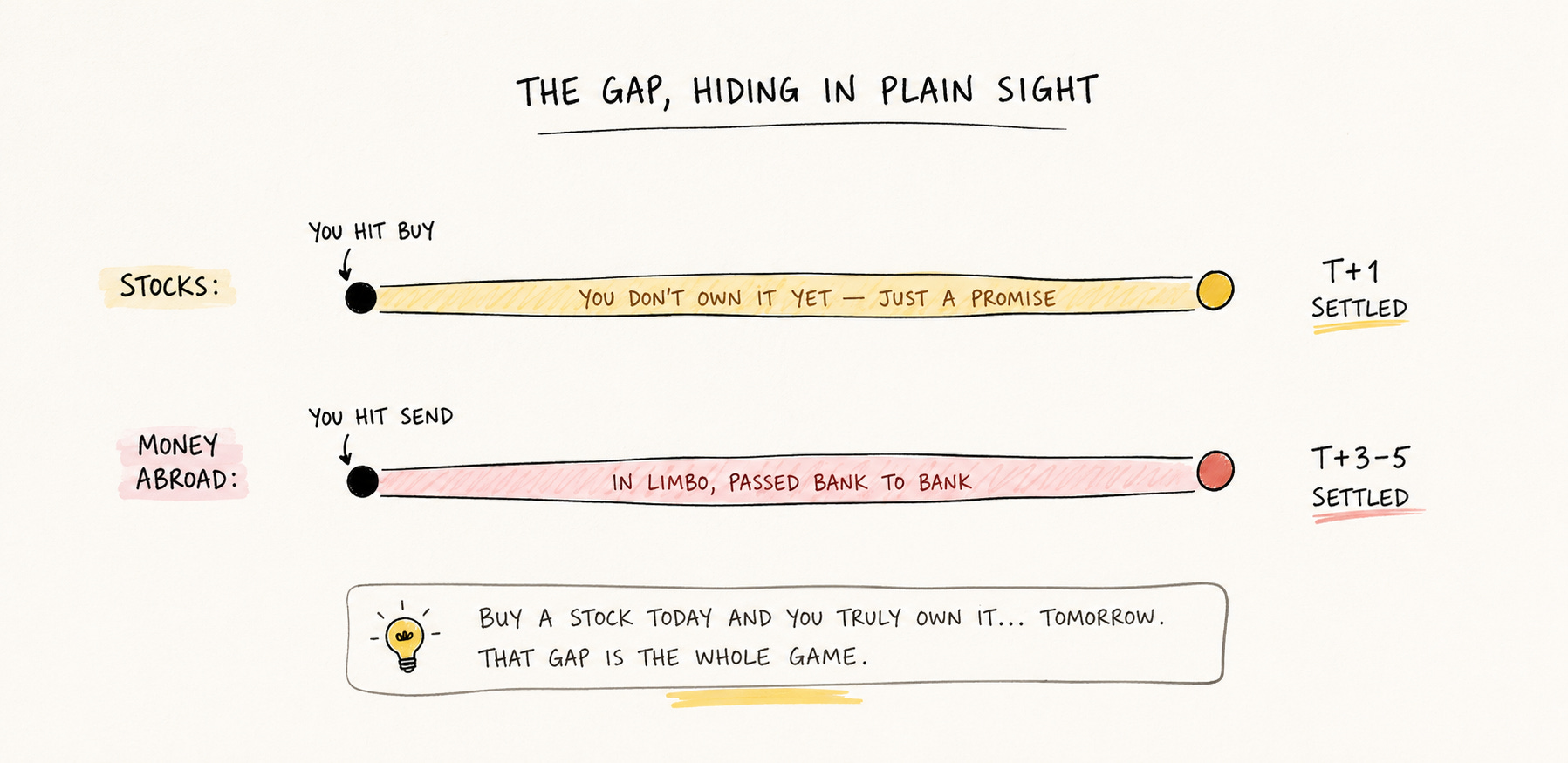

Buy a share of a US company today, and the trade doesnt truly settle until the next business day. Its called “T+1” - trade date, plus one day. For a full day, you dont actually own that stock. You own a promise, tracked by a giant clearinghouse. (And it used to be worse - it was two days, T+2, until 2024.) Send money across a border, and its often 3 to 5 days, crawling through a chain of banks, exactly the kind of toll-road delay we measured in What 180 Currencies Actually Cost.

Why does the gap exist at all? Mostly legacy. The old system bundles up everyones promises and settles them later, in batches, during business hours, using technology built decades ago. It works but that open gap, it turns out, is where the danger lives.

Why the gap is quietly dangerous

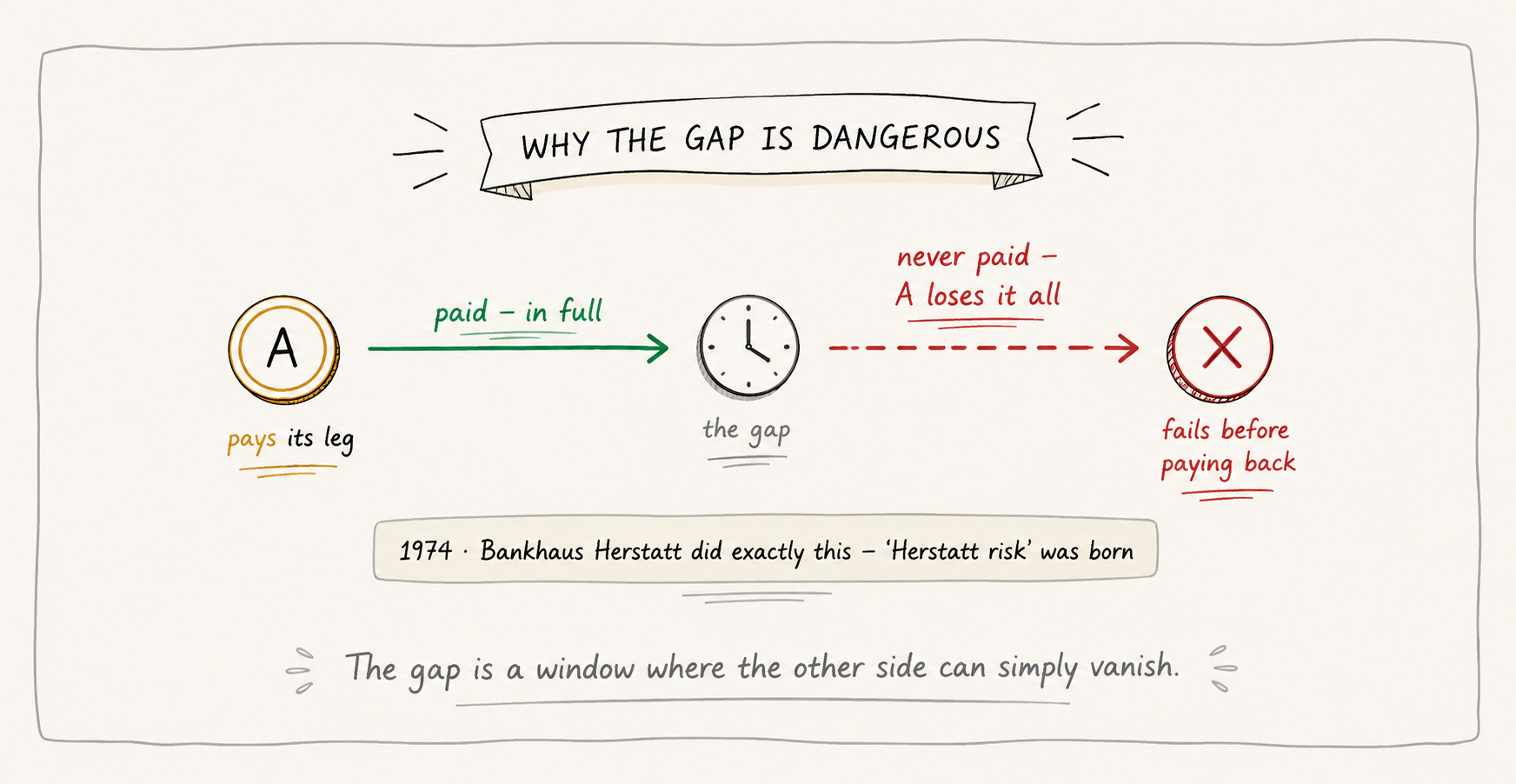

Heres the thing about a gap between the promise and the payment: its a window. And in that window, the other side can vanish.

The most famous example is a small German bank called Bankhaus Herstatt. In 1974, it had taken in payments in one currency from banks around the world but before it paid out the other side of those deals, regulators shut it down. The clock had been ticking across time zones, and the gap caught everyone. The banks that had already paid their leg simply... lost it. The other side never came. It was such a clean illustration of the danger that the industry named the risk after it: Herstatt risk.

This is the dirty secret of the old settlement system: the gap creates risk, and that risk has to be managed expensively. The entire towering edifice of clearinghouses, central counterparties, collateral, and special settlement systems exists for one reason: to stand in the middle of that gap and absorb the danger of someone failing before the deal becomes real. We touched the central-bank side of this machinery in How Central Banks Actually Control Inflation this is its plumbing.

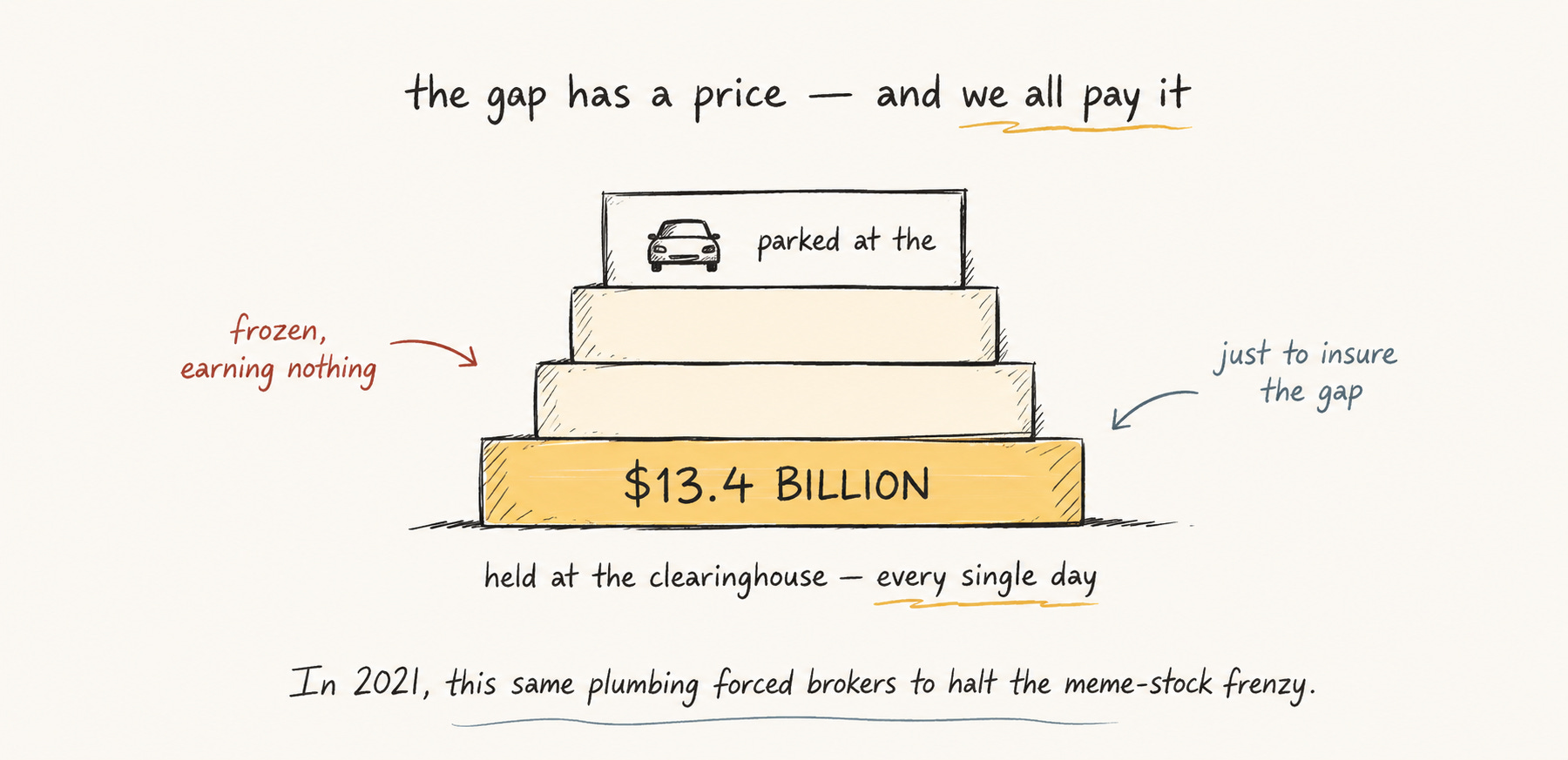

The gap has a price, and we all pay it

That safety doesnt come free. To cover the risk of someone failing during the settlement window, the main US clearinghouse holds an average of more than $13.4 billion in margin every single day. Thats billions of dollars, frozen, sitting idle, doing nothing productive, purely as a buffer against the gap. And thats just one clearinghouse; across the whole system, the trapped collateral runs into the trillions.

And once in a while, the public actually sees this hidden plumbing crack. Remember the meme-stock frenzy of 2021, when brokers suddenly froze buying and everyone screamed “censorship”? The real culprit was far more boring and far more revealing: during that two-day settlement gap, the clearinghouse demanded huge extra collateral to cover the wild volatility, and some brokers simply couldnt post it fast enough so they had to halt. That wasnt a conspiracy. That was settlement mechanics, live on national television. The gap, biting.

The fix: closing the gap to zero

So heres the obvious question. If the gap is the source of all this risk and trapped money... why not just close it? Make settlement instant?

For decades, the honest answer was: we cant, the technology cant do it. Shrinking the gap from two days to one (the 2024 move to T+1) alone cut the required safety margin by roughly 41%, which tells you how much risk lives in time. But going all the way to zero instant, final settlement was simply impossible with the old batch-processing pipes. “Something would have to shift,” the industry kept saying.

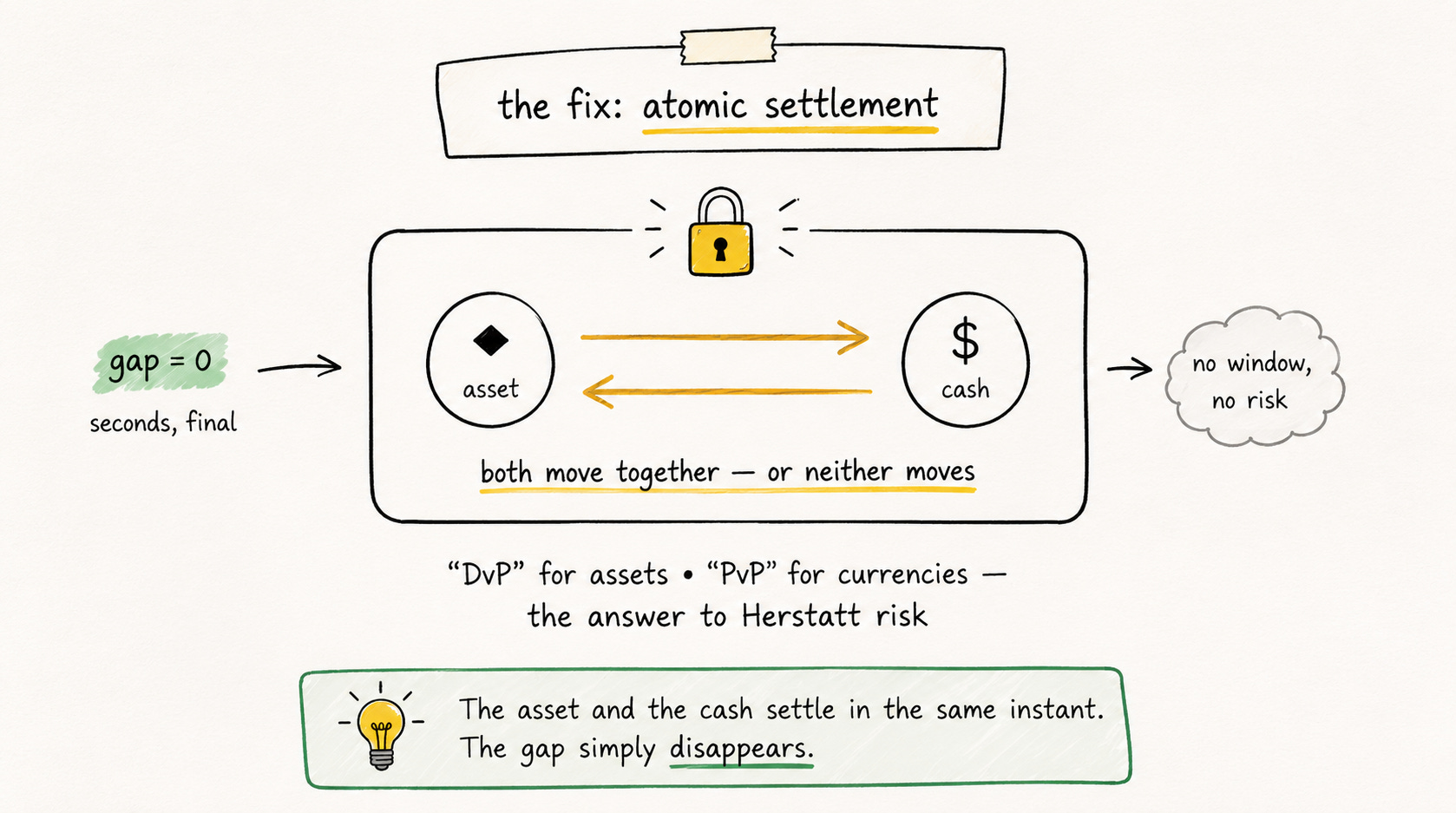

That something has arrived, and it has a name: atomic settlement. “Atomic” means all-or-nothing, in a single instant. The asset and the cash move at the exact same moment, locked together in one transaction or neither moves at all. The buyer gets the asset the precise instant the seller gets the money. The gap doesnt get shorter. It collapses to zero. No window. No Herstatt risk. Nothing to fail in between.

The old world had a name for the ideal “delivery versus payment,” or DvP for assets, and “payment versus payment,” PvP, for currencies and it has chased it since the 1980s. What changed in 2026 is that its finally, technically achievable, because both the money and the asset can now live as software on the same programmable ledger. And that ledger - the thing that holds the final, shared, irreversible record of who owns what - is exactly what a blockchain is, underneath all the noise about coins.

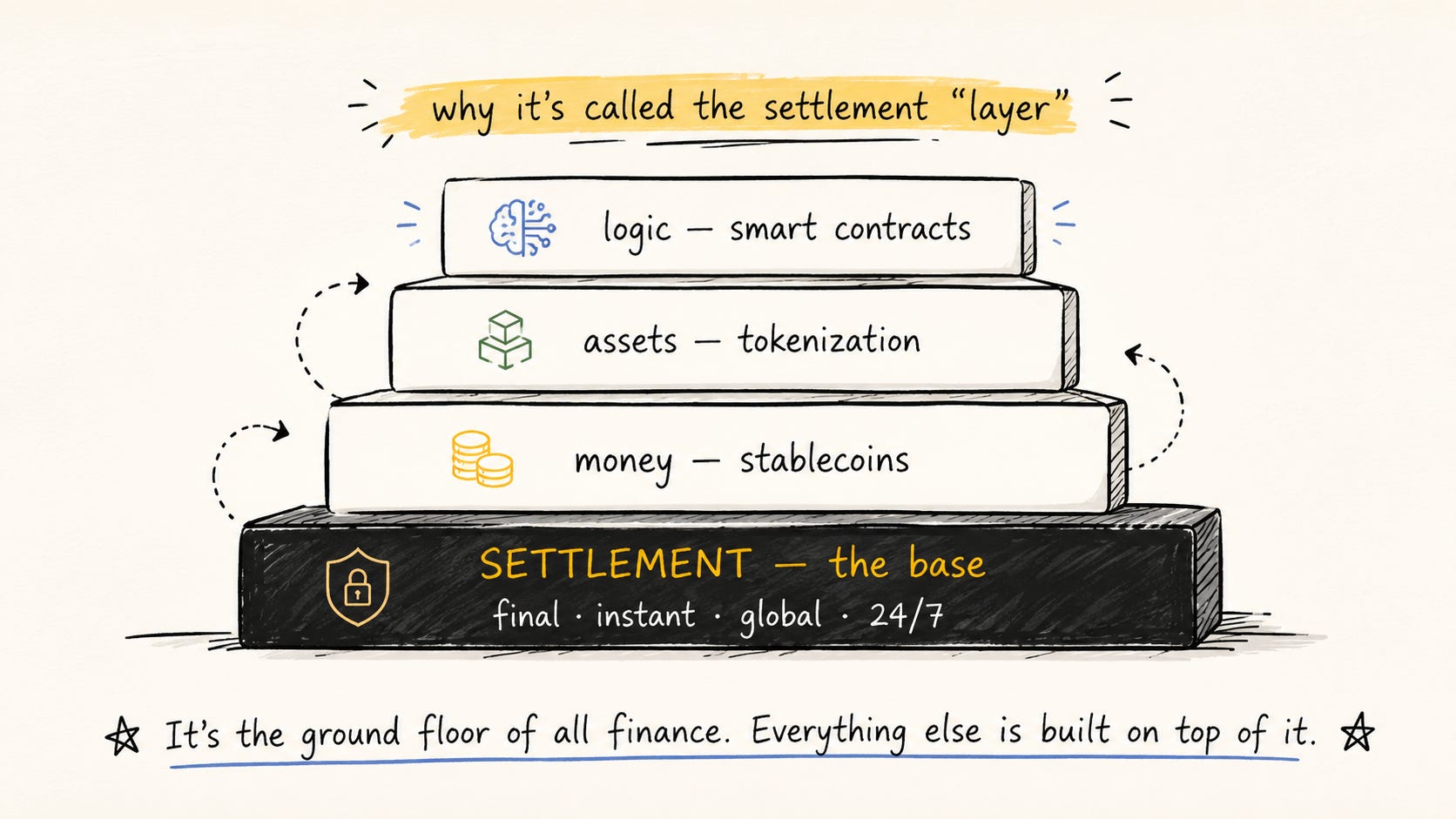

Why it’s called the settlement “layer”

Now the phrase makes sense. In the four-floor stack we mapped in the last piece - settlement at the bottom, then money, then assets, then logic on top - the settlement layer is the ground floor. Its the bedrock the entire building stands on. Get final, instant, global settlement right, and everything above it - payments, tokenized assets, programmable finance can be built on solid ground. Get it wrong, and the whole structure wobbles on a multi-day gap full of risk.

Thats why “settlement layer” isnt jargon. Its the most foundational concept in the entire rebuild. Its the floor.

Who’s actually building this

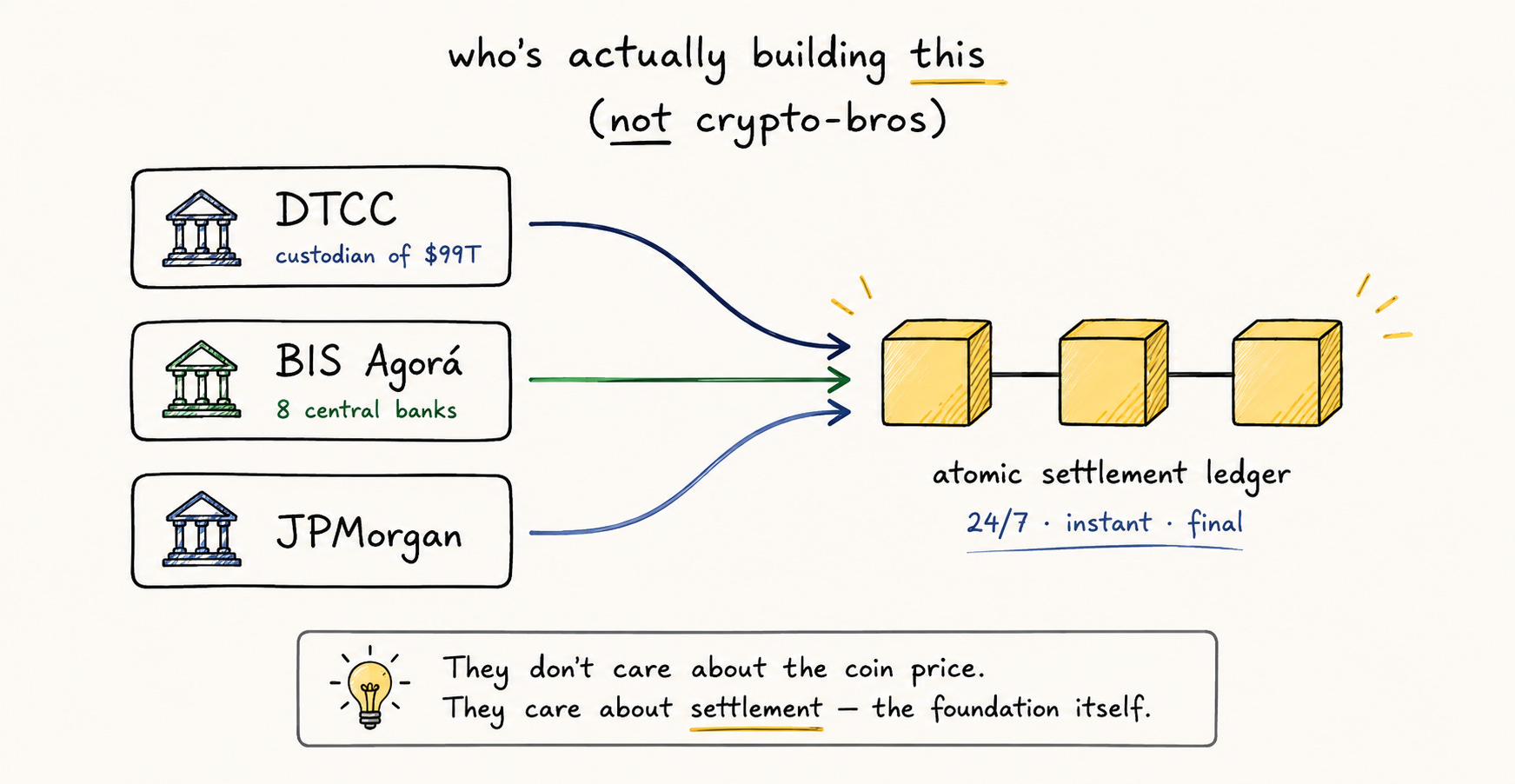

And heres how you know this is real and not crypto hype: look at who is building it. Not anonymous coin traders. The most conservative, systemically important institutions on the planet and theyre not doing it for the price of any coin. Theyre doing it for settlement.

The DTCC - the clearinghouse that provides custody for securities worth around $99 trillion got regulatory clearance to run a tokenized-settlement pilot for stocks, ETFs, and US Treasuries, explicitly to enable on-chain atomic settlement, 24/7, including weekends. And the central banks themselves are in it: the Bank for International Settlements is running Project Agorá, which brings together eight central banks (covering the major reserve currencies) and more than 40 of the worlds biggest financial institutions to build a single shared platform for atomic, multi-currency settlement across borders, around the clock. JPMorgan is settling with deposit tokens. The list goes on.

When the custodian of $99 trillion and eight central banks are quietly rebuilding the foundation of finance on this exact technology, the “is blockchain useful?” debate is simply over. They could not care less about the casino. They care about the settlement layer - the foundation itself.

Why this is the One Earth, One Currency story

Now step all the way back and see what these institutions are actually building. A single, shared, global ledger where money and assets in many currencies settle instantly and finally, across borders, 24/7, for everyone plugged in.

Sit with that, because Project Agorá - central banks and global banks all settling together on one shared programmable platform is, almost word for word, the blueprint of the thesis this whole newsletter is built on. The settlement layer is the deepest, most foundational floor of One Earth, One Currency. Not one coin. Not one ruler. Just one shared settlement fabric the whole world can plug into - the literal bedrock on which a single, connected financial system gets built. We watched the banks bolt onto these rails even as prices crashed in Crypto Was Supposed to Escape the System, and saw your own bank already quietly using them in Your Bank Is Already Using DeFi. This is the floor underneath all of it.

Your settlement x-ray - keep this

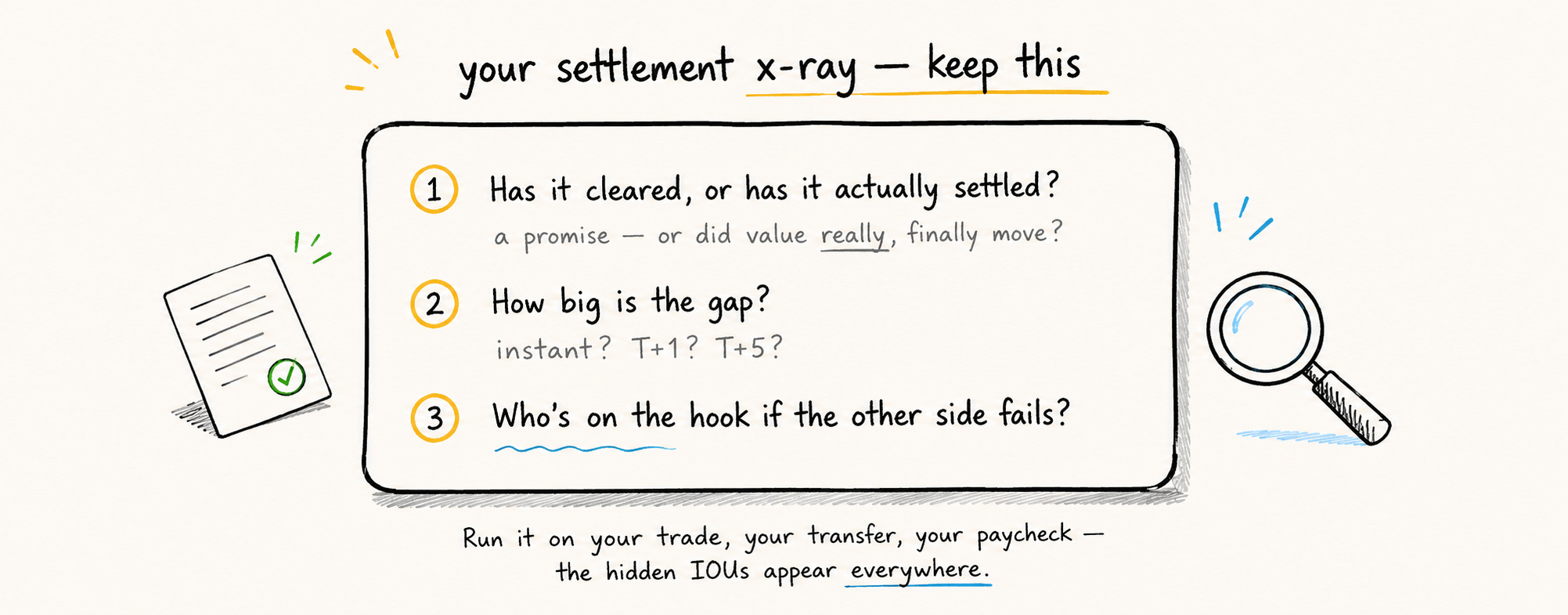

So heres the tangible thing to walk away with - a lens that lets you see this hidden gap everywhere, for the rest of your life. From now on, whenever value is supposed to “move” a stock trade, a bank transfer, your paycheck, a payment to a friend - dont take it at face value. X-ray it with three questions:

1. Has it cleared, or has it actually settled? Is this still just a promise - an IOU, a “pending” or did value really, finally, irreversibly move?

2. How big is the gap? Is it instant? T+1? Three to five days? The length of that gap is the length of the risk.

3. Who’s on the hook if the other side fails during the gap? Theres always someone standing in that window, absorbing the danger - a clearinghouse, a bank, sometimes quietly you.

Run that x-ray on your own financial life and youll start seeing the invisible IOUs and risk windows hiding inside things you always assumed were instant and done. Thats not a stock tip. Its a way of seeing and its yours now.

The whole point

Settlement sounds like the most forgettable word in finance. Its actually the floor the whole house is built on, the moment a promise becomes real. The old system left a gap between those two things: a gap measured in days, filled with risk, plugged with billions in idle collateral, that occasionally cracks in public. The new settlement layer closes that gap to zero - instant, final, shared, global which is exactly why the most serious institutions on earth, central banks included, are quietly rebuilding finance from this layer up.

So the next time someone “sends you money,” youll know to ask the only question that really matters: did it actually move or are you just holding a promise across a gap? Thats the whole game. And the new rails are quietly closing the gap to nothing.

Thats the foundation. Next, we keep climbing the stack. See you in the next one.

Keep going

Your Bank Is Already Using DeFi. They Just Won’t Tell You. — the new rails this settlement layer is built into.

Crypto Was Supposed to Escape the System. It’s Becoming It. — why the institutions care about settlement, not the price.

One Planet, 180 Currencies. Something’s Off. — the One Earth, One Currency vision this is the bedrock of.

Naked Market exists to close the gap between what’s actually happening in global finance and what eventually makes it to the headlines. If you want to understand the foundation being rebuilt before it becomes obvious - subscribe and we’ll keep going.

- More Soon